Commodity markets have a habit of reminding us that supply chains do not break neatly. When geopolitics disrupts oil and gas, the effects rarely stay confined to energy. This time aluminium has been one of the clearest casualties, as the market confronts the risk that Gulf smelters could struggle both to ship metal out and to keep raw materials and energy flowing in.

Aluminium catches a geopolitical premium

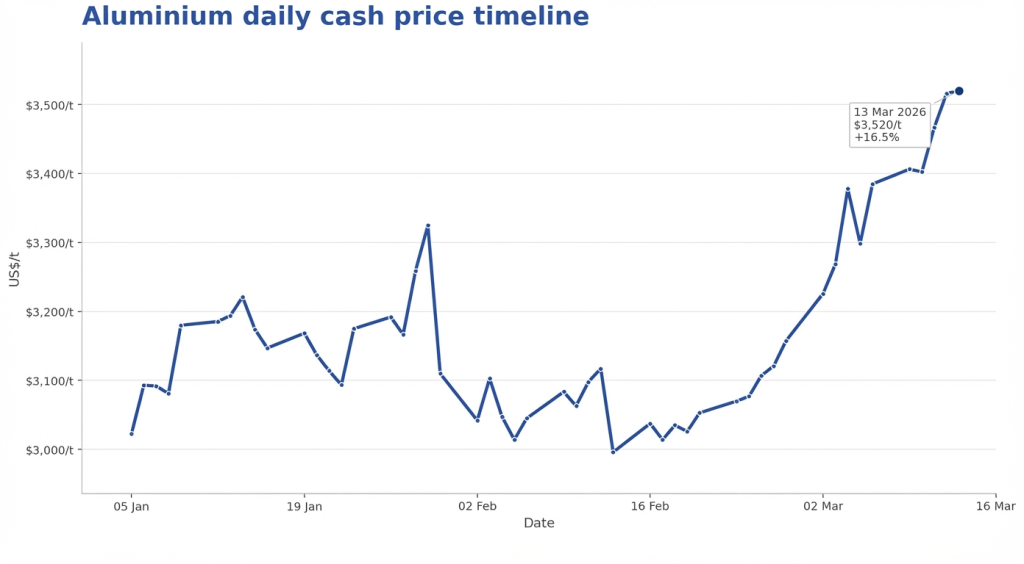

For aluminium prices, the move has been sharp and unusually persistent. LME prices rose from US$2,996/t on 13 February 2026 to US$3,520/t on 13 March 2026, a gain of 17.5%. From 2 March to 13 March alone, aluminium moved from US$3,226/t to US$3,520/t, up 9.1%.

The market was already firm through January, weakened into mid-February, and then turned decisively higher as Gulf disruption moved from risk scenario to operating reality. That sequence matters. Aluminium did not simply spike on headlines. It repriced and held near the highs, suggesting the market believes disruption may last longer than the initial jubilation.

The scale of the move reflects more than general nervousness in commodities. Aluminium has rallied because the market is now attaching a higher probability to real supply-chain interruption. The Gulf is a major source of primary aluminium for Europe, Asia and other import-dependent regions. Once buyers started to doubt whether those tonnes would flow normally, and whether the region’s smelters could keep operating at normal rates, the cash market moved quickly to price scarcity rather than inconvenience.

Hormuz matters more than many buyers realised

The Strait of Hormuz is usually discussed in oil and LNG terms, but it is just as important for aluminium. More than 5Mt of aluminium move each year through the corridor from smelters in Bahrain, Qatar, Saudi Arabia and the UAE, while bauxite and alumina move in the opposite direction to feed those plants.

That is why the market response has gone beyond a standard freight premium. If the issue were limited to delayed outbound shipments, the effect might have been narrower and more temporary. But once feedstock vessels began diverting away from Gulf destinations, the market had to consider a second and more serious risk: disruption to ongoing production. Aluminium smelters are not designed to absorb prolonged uncertainty comfortably. The longer the disruption lasts, the more the market starts to think not about late cargoes, but about lost tonnes.

That two-way dependency is what makes the current disruption so important. Hormuz is not simply an export route for finished metal. It is part of the production system itself.

A concentrated Gulf supply base

The Gulf aluminium system is concentrated in a handful of large, export-oriented smelters. EGA’s pre-war production was operating at an annualised run-rate of roughly 2.7Mt, while Alba produced a record 1.6Mt in 2025. Qatalum’s nameplate capacity is about 648kt, while Sohar Aluminium’s capacity is about 395kt. Saudi Arabia adds another major block through Maaden. The result is a regional supply base dominated by a handful of large, export-oriented smelters.

In normal markets, that concentration helps make the region one of the world’s most efficient aluminium exporters. In stressed markets, it means disruption can affect a large share of regional output at once. The market is therefore not reacting to a fringe producer being squeezed. It is reacting to a meaningful portion of global seaborne supply becoming less reliable.

The bottleneck runs both ways

The deeper vulnerability is that the Gulf is much stronger in smelting than it is upstream. The region is a major producer of primary aluminium, but far less significant in alumina and bauxite.

Once bauxite and alumina cargoes started diverting away from Gulf destinations, aluminium ceased to be just an export story. The market had to start asking how long smelters could maintain output if feedstock flows no longer arrived on schedule.

Operational strain starts to show

Qatalum began a controlled shutdown process earlier in March after a gas-related disruption, before stabilising at around 60% capacity once reduced gas supply was stabilised. That still leaves the market short of meaningful output relative to normal conditions.

Alba has moved further still. What began as a shipping problem severe enough to trigger force majeure has developed into a controlled shutdown of Lines 1, 2 and 3, equivalent to 19% of total capacity. That progression shows how quickly a logistics problem can become a production problem.

Premiums tell the real story

The LME price has moved sharply, but the physical market has tightened even more visibly. European duty-paid premiums have risen to around US$420/t, while the US Midwest premium has reached around US$2,400/t.

Warehouse behaviour reinforces the same point. Large tonnages of aluminium have been cancelled for withdrawal from LME warehouses in Port Klang, and cancelled warrants have jumped sharply since late February.

Why the market is paying up

The structural issue is straightforward. The GCC matters a great deal in primary aluminium, but much less in the feedstocks that sit upstream of that metal.

Because of that mismatch, the disruption affects both sides of the equation. Metal becomes harder to ship out just as inputs become harder to bring in, and nearby units naturally become more valuable.

What happens next?

The next phase of the move will depend on duration. If disruption in and around Hormuz eases quickly, rerouted cargoes, smelter inventories and non-Gulf supply may help stabilise the market. But if disruption persists, feedstock risk rises and nearby metal remains scarce.

The main counterweight is demand. A sufficiently large slowdown in industrial activity could offset some of the supply shock. For now, though, the balance of evidence still points to supply disruption as the dominant force behind the move in aluminium.

For now, aluminium has become a geopolitical metal

The broader lesson is that the market had become too comfortable with Gulf aluminium as stable, flexible export supply. That assumption is now being corrected. Aluminium remains the metal of transport, packaging, construction, wiring and electrification. But for now, it is also trading like a geopolitical metal. Its availability depends on whether Hormuz can function, whether feedstock cargoes can still reach Gulf smelters and whether disrupted tonnes can be replaced quickly enough elsewhere. That is why LME aluminium has moved so sharply, and why the market remains vulnerable if the disruption persists

Leave a comment