Energy markets have a habit of reminding us—often abruptly—that they are less a set of independent commodity markets and more a tightly connected ecosystem. Pull hard enough on one thread and the whole tapestry shifts.

The latest reminder arrived at the end of February when the United States–Iran conflict sent tremors through global energy supply chains. Oil reacted first, LNG followed close behind, and within days thermal coal—supposedly the fading relic of the energy transition—was staging a rather unambiguous comeback.

If energy markets had a sense of humour, they might call it coal’s revenge.

Oil fires the starting gun

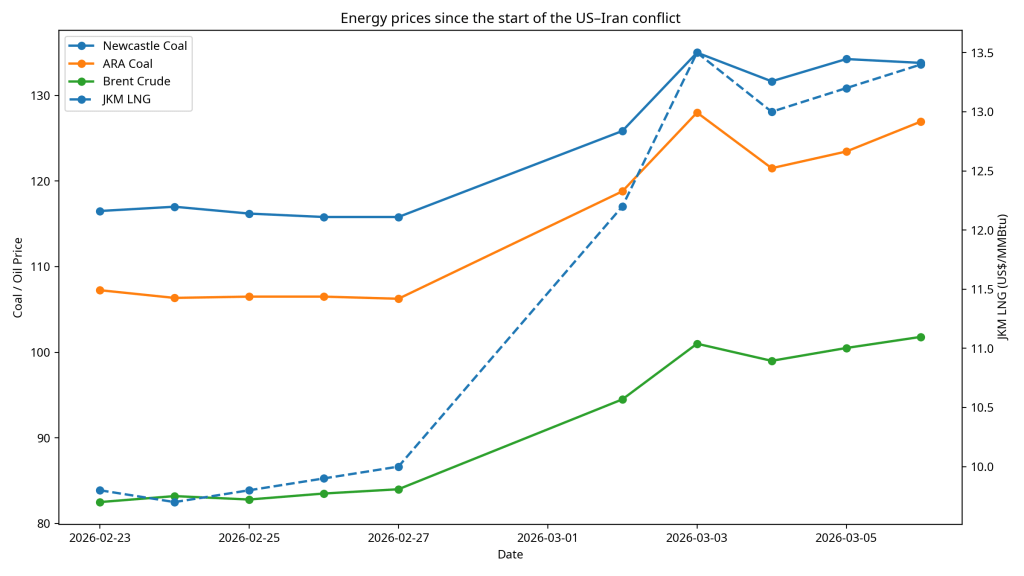

The initial shock, unsurprisingly, was in crude oil. Brent crude jumped from the mid-$80s/bbl before the conflict to around $100/bbl within a matter of days. The move had less to do with immediate physical disruption and more with a familiar geopolitical pressure point: the Strait of Hormuz.

Roughly one fifth of global oil trade and a substantial share of LNG shipments pass through the strait, meaning any conflict involving Iran inevitably introduces a risk premium to energy markets. Even the possibility of disruption is enough to send traders scrambling to price in worst-case scenarios.

Oil therefore acted as the market’s early warning signal. But the real story quickly shifted to natural gas.

LNG tightens—and power markets start to sweat

LNG markets were already operating with limited slack. The prospect of shipping disruptions in the Gulf pushed the JKM LNG benchmark from roughly $10/MMBtu to the low-$13/MMBtu range within the first week of the crisis.

For global power markets, that matters enormously.

Natural gas increasingly sits at the centre of marginal electricity pricing in many regions. When LNG prices rise sharply, the cost of gas-fired generation rises with them. Utilities suddenly start looking around for cheaper electrons—and in many systems there is only one alternative fuel capable of stepping in quickly.

Coal quietly rallies

Thermal coal prices moved with surprising speed.

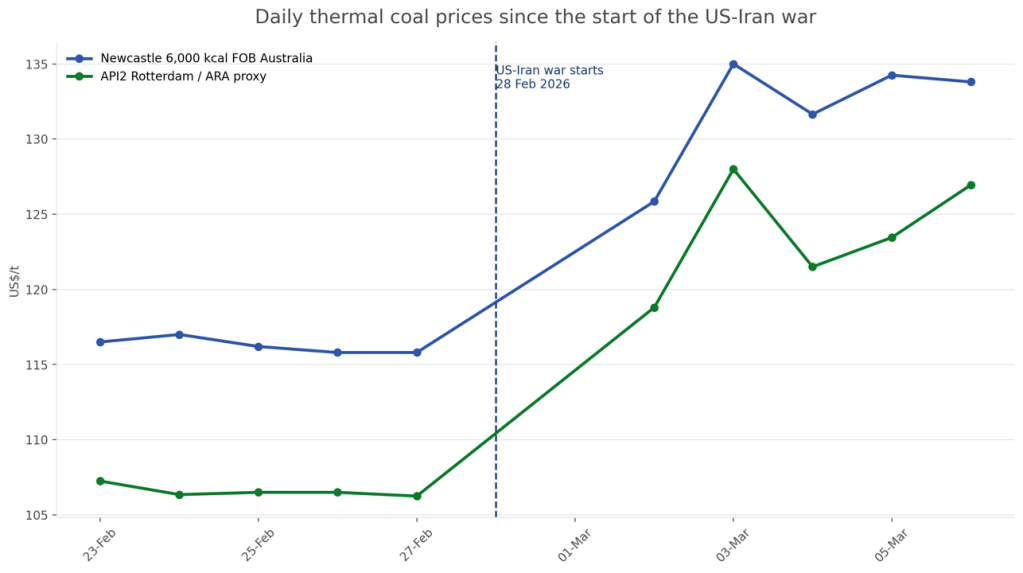

The Newcastle 6,000 kcal benchmark climbed from around $116/t before the conflict to roughly $134/t, a gain of around 15% in just over a week.

In Europe, the response was even stronger. The ARA benchmark rose from roughly $106/t to around $127/t, close to a 20% increase over the same period.

This wasn’t about coal supply disruptions. Mines kept operating, and shipping routes for coal were largely unaffected.

Instead, the rally reflected a simple reality of power markets: when gas gets expensive, coal becomes competitive again.

Even in systems that are steadily decarbonising, a fleet of coal-fired plants often remains on standby. When the economics flip, they can return to dispatch with remarkable speed.

The fuel-switching reflex

The mechanism driving the rally is well known but often underestimated.

When LNG prices spike, utilities with dual-fuel capability begin shifting generation toward coal. The result is a rapid increase in seaborne coal demand, particularly in regions where coal plants remain operational but underutilised.

Europe is particularly sensitive to this dynamic. Since the restructuring of its gas supply following the Russia–Ukraine war earlier in the decade, the region has relied heavily on LNG imports. That makes European power prices—and by extension coal demand—highly responsive to LNG market shocks.

Hence the stronger rally in the Atlantic coal market (ARA) relative to the Newcastle.

In other words, gas sneezed and coal caught a cold—albeit a profitable one.

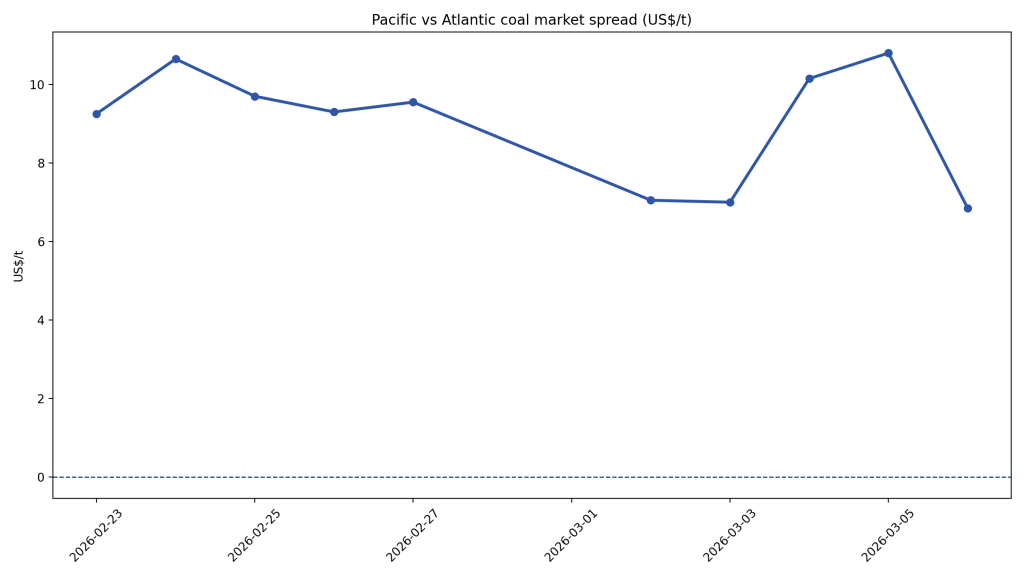

Atlantic and Pacific markets move together

Another notable feature of the recent price movement is the synchronisation of coal markets.

Historically, the Atlantic basin and Pacific basin coal markets often diverge depending on regional demand patterns. Asian power demand might tighten Newcastle prices while European coal remains soft, or vice versa.

This time both markets moved higher together.

The Atlantic rally was driven primarily by gas-to-coal switching in Europe, while the Pacific market received support from Asian utilities securing additional supply amid broader energy market uncertainty.

The result was a global coal rally rather than a regional one.

Energy markets remain deeply interconnected

What the episode ultimately illustrates is the degree to which energy commodities remain intertwined.

A simplified chain of events looks something like this:

- Geopolitical tension raises oil prices.

- Shipping risk and supply concerns tighten LNG markets.

- Higher gas prices increase power generation costs.

- Utilities shift toward coal.

- Coal prices rally.

The coal market therefore didn’t react to coal fundamentals so much as respond to the physics of the power system.

When gas becomes expensive, electrons still need to come from somewhere.

Coal’s stubborn role in energy security

The episode also offers a reminder of something policymakers occasionally prefer to ignore: coal remains an important part of the global energy system’s safety net.

Even as renewable capacity grows rapidly, many power systems still rely on coal plants as dispatchable backup during periods of fuel scarcity or extreme demand.

In calm markets that capacity may sit idle. But during geopolitical shocks or supply disruptions, coal’s role becomes immediately apparent.

The past week’s price movements demonstrate just how quickly that role can re-emerge.

What happens next?

Whether coal’s rally persists will depend largely on the trajectory of the broader energy market.

Several factors will be critical:

- The duration and intensity of the US–Iran conflict

- Whether shipping through the Strait of Hormuz remains uninterrupted

- LNG cargo availability outside the Gulf

- Utility coal stock levels entering the northern hemisphere summer

If LNG prices remain elevated, coal demand could stay firm for some time.

But if geopolitical tensions ease and gas prices retreat, coal markets may give back some of their recent gains.

For now, the old fuel still has teeth

Energy transitions rarely move in straight lines.

For the better part of a decade coal has been cast as the fading incumbent of the energy system. Yet every so often the market reminds us that the world’s energy infrastructure evolves slowly—and that reliability still matters.

The latest Middle East crisis delivered precisely that reminder.

And for a brief moment at least, the black rock found itself back in the driver’s seat of the global power stack.

Leave a comment